Roth IRA Conversions─Do They Make Sense?

— The Answer Will Shock You! —

If you would like to know if a Roth IRA conversion makes sense for your individual situation, please contact our office. We have proprietary conversion software so we can tell you in a matter of minutes if converting will make sense. E-mail info@thewpi.org or call 269-216-9978 to set up a time to come in and have your numbers calculated.

What is a Roth IRA conversion?

It’s simply when you convert a traditional tax-deferred IRA to a Roth IRA where, once converted, the money is allowed to grow tax-free and come out tax-free. Income taxes are due on ALL of the money in the IRA at the time of conversion. If you convert before age 59.5, the normal 10% penalty for early withdrawal is waived so long as you wait 5 years before taking money out of the new Roth IRA and are over 59.5 when taking withdrawals.

Should you convert your traditional IRA to a Roth IRA?

The answer depends. On what? More variables than you can shake a stick at (which is why we use proprietary software to calculate the number.

As a general statement that, if you are in the same or lower tax bracket when in retirement, converting to a Roth IRA is NOT going to make economic sense.

Examples

The best way to get the point across is with examples. For the examples, we will convert a $500,000 IRA. We used a 1.2% average mutual fund expense on the money in the IRA and a 7% annual rate of return. We will have the clients take income at age 70 for 15 years. We assumed the client’s file taxes as married filing jointly and lives in a state with NO income tax.

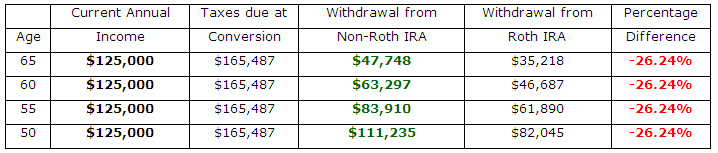

1) Paying income taxes from the IRA—This example is for someone who does not have “other money” to pay the income taxes due when converting the traditional IRA to a Roth IRA.

The above charts make it clear that, if you are planning to use the money from your IRA to pay the income taxes for the conversion, it’s going to make little sense to convert. We assumed the example client would be in the same income tax bracket in retirement.

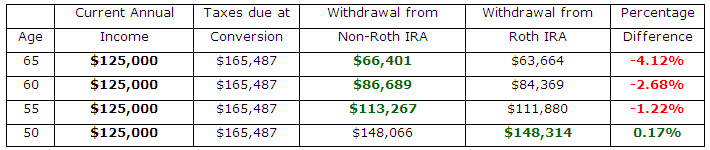

2) Paying taxes due on conversion from “other” non-IRA sources—the following examples assume that there are sufficient “other funds” (cash in the first example) that can be used to pay the income taxes upon conversion (so all of the money upon conversion can stay in the new Roth IRA to grow and come out tax-free).

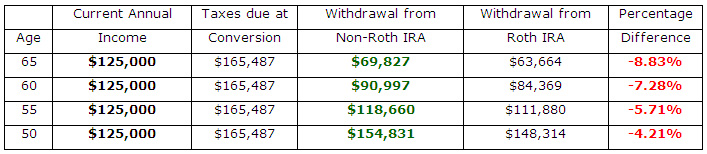

The following is if the client had to sell stock with a $50,000 basis to pay the tax and where the mix of long-term and short-term capital gains taxes upon the sale is 50%.

Going up in income tax-brackets in retirement

Many people think that income taxes will rise in the coming years. While no one has a crystal ball, we wanted to let you know that if your income tax bracket is higher in retirement, the numbers supporting a Roth Conversion is increased. If you take the last chart and assume the client’s income tax rate went up to 35% in retirement, the percentage difference in how much after-tax income would be available would look as follows: age 65: +1.01%; 60:+2.88%; 55: +4.77%; 50: +6.59%.

Summary

The theory of a converting a traditional IRA to a Roth sounds great when you think about it really quickly (pay taxes now so money can grow for years tax-free and come out tax-free in retirement). However, when you factor in ALL the needed variables, you will find that unless you plan on being in a higher (or much higher) income tax bracket in retirement, converting your traditional IRA to a Roth IRA will make little economic sense.